Bukas Finance Corp. is a duly registered Financing Company with SEC registration No. CS201901691 and Certificate of Authority No. 1199.

Please remember to study the Terms and Conditions in the Disclosure Statement before proceeding with any loan transaction.

The First 3 Questions to Ask Before Getting a Student Loan in the Philippines

If you’re exploring ways to pay for college, taking out a student loan (or a tuition installment plan) is one option. Since most students in the Philippines are unfamiliar with how student loans or installment plans work, we’ll highlight three important questions to ask before getting one.

(1) Principal or Loan amount: How much am I borrowing? (Magkano ang kailangan kong hiramin na pera?)

The principal amount is the total amount of money you are borrowing right now. You will pay this amount back in the future. Instead of needing the full tuition at the start of the semester, you can pay it back later in smaller amounts.

While this option is more flexible, remember that student loans or installment plans charge interest rates and fees in exchange for this service.

(2) Interest rates and other fees: How much do I have to pay back? (Magkano ang babayaran ko?)

Besides the principal amount (item #1), you have to be aware of the interest rates and other fees that your lender charges. Adding these items together will result in the total amount you have to pay back.

Interest rate is the percentage of the principal you have to pay your lender in exchange for borrowing money. The simple way to calculate the interest you owe is multiplying the interest rate by the total amount borrowed. We’ll cover other forms of interest soon, so stay tuned!

There are other fees a lender may charge. These fees include the processing cost (also called origination fee or service fee), or the penalties if you pay late (late fee). It’s important to be aware of all applicable fees to get a complete picture of how much you’re paying! You can check the complete details of your plan including a list of fees by reading your contract or going through the disclosure statement. Make sure you review and fully understand these terms before you make any commitments!

(3) Repayments and Installments: When do I have to pay it back? (Kailan ko kailangan bayaran ito?)

Now that you know how much you have to pay, when do you actually have to pay the loan/plan (plus interest and fees) back? While the terms vary depending on the loan, there are two conditions:

- Frequency - how often do I have to pay it back? (Gaano kadalas kailangan magbayad?)

- Maturity - until when do I have to pay? (Hanggang kailan ko kailangan magbayad?)

For student loans, installment plans (or hulugan) are common. A typical plan requires you to pay once a month (frequency) for one year (maturity). This means you have to pay twelve times. The advantage of installment plans is you turn your tuition into bite-sized payments (versus a large one-time payment).

Note that some student loans and installment plans allow you to repay the loan amount earlier (also known as early repayment). Depending on the lender, you may be able to get rewards for paying ahead of schedule.

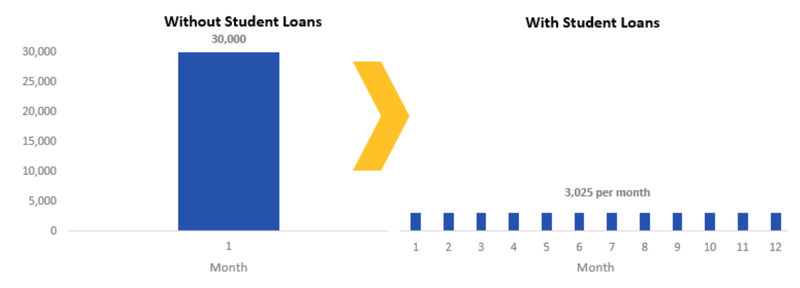

Applying everything we’ve talked about so far, here’s an example of what a student loan or installment plan will look like versus paying upfront.

- Principal Amount: P30,000

- Interest and Other Fees:Interest Rate: 1.5% flat rate per month = 1.5% x 12 months = 18%

- One-time Service Fee: 3%

- Installment: Payable in 12 monthly installments

- Computation of Total Amount Due: P30,000 x (1 + 18% + 3%) = P30,000 x 1.21 = P36,300 or P3,025 per month

After you familiarize yourself with these crucial terms and questions, you’re on your way to making an informed financial decision! Before you decide on an installment plan or student loan, we do recommend being aware of all your alternatives. At Bukas, we provide flexible tuition installment plans to college and postgraduate students from our official partner schools (FEU Manila/Makati/Tech, Mapua Manila/Makati, NTC, EAC Manila, JRU, LPU Manila/Makati and OLFU Antipolo/QC/Valenzuela). We’re always here as your financial partner, and we’re determined to help you complete your education.

Want to learn more about alternative payment options for your tuition? Follow us on Facebook, Twitter and Youtube or Register at Bukas.

This post is part of a series of articles to promote Financial Literacy in the Philippines. If you need financial advice or have some related questions, feel free to send us a message on Facebook and we'll try to help you.

______________________________

About the Author

Riche Lim is a graduate student at the Stanford Graduate School of Business. He previously led the equity research team of BPI Securities, and was a former finance and accounting lecturer at Ateneo de Manila University. His other work experiences include investment banking at J.P Morgan in San Francisco, and strategy at Sea in Singapore.